Your service protects people from real financial loss. But getting clients? You’re either paying lead aggregators, running expensive Google Ads, or waiting on referrals you can’t control.

That’s a fragile foundation for a business that delivers real value.

Referrals don’t scale. Paid leads eat into margins. Neither builds anything permanent. SEO is how insurance brokers build the alternative: consistent, compounding, organic client acquisition that doesn’t cost per lead and doesn’t stop working when the budget does.

Here’s how it works, what it costs, and how to find an agency that actually knows this niche.

What SEO for Insurance Brokers Includes and Why You Need Each One

Insurance SEO is made up of four components that work together. Each one serves a distinct function, and skipping any one of them limits what the others can achieve. Here’s what each involves and why it matters for your business.

1. A Technically Strong, UX-Focused Website That Google, AI Search Models, and Your Visitors Can Trust

Before you start working on SEO, the website itself has to be built right. Google, AI search engines, and your prospects all assess your site before they engage with it. If the technical foundation or the user experience is weak, rankings and conversions both suffer.

Technical requirements:

- Fast load time on desktop and mobile (under 3 seconds)

- Mobile-responsive design because most insurance prospects search on a phone

- Clean site architecture that Google’s crawler can read without issues

- Correct indexing setup: XML sitemap, robots.txt, no broken pages or redirect chains

- Core Web Vitals compliance (Google’s page experience signals)

Navigation and core page structure:

The main navigation should be simple and purposeful:

- Home → clear positioning, primary service, and location signal

- Services → one dedicated page per service type (commercial liability, professional indemnity, life insurance, health cover, etc.)

- About → establishes trust and credibility, critical in a YMYL niche

- Contact → accessible from every page, with click-to-call on mobile

Every service page needs to target a specific query. Generic “insurance services” overview pages don’t rank for anything useful.

2. An SEO and Content Strategy Built Around What Your Prospects Search For

Once the website foundation is in place, the next step is deciding which pages to build and which keywords to target. This is where most brokers, and most agencies, get it wrong — targeting terms that are impossible to win or producing content with no strategic direction.

A proper insurance SEO content strategy covers three layers:

- Sub-service pages

One page per specific service type: commercial liability, professional indemnity, life insurance, health cover, and so on. Each page targets a distinct keyword and serves a distinct prospect. A single generic services page ranks for nothing specific.

- Location pages

One page per target market: “commercial insurance broker in [city]” or “business insurance for [city] contractors.” These are the pages that win local search and map pack visibility. You will need Google Business Profile optimisation as well because an optimised GBP with consistent directory listings and genuine reviews is often the highest-return local SEO move for an independent broker.

- Blog and educational content

Posts that answer questions your prospects are searching before they’re ready to contact anyone: “do I need public liability insurance,” “what does an umbrella policy cover,” “how much does professional indemnity cost.” These build topical authority and pull in prospects earlier in the decision process.

3. Content Creation That Meets the Standards Google Sets for Insurance

Content in a YMYL niche is evaluated differently than a lifestyle blog or a home services site. Thin, generic, or inaccurate content does not rank in insurance, regardless of how well the page is otherwise optimised.

What this means:

- Every service page and blog post must be accurate to the specific coverage type it covers

- Writing must reflect genuine industry knowledge, not just keyword targeting

- Claims need to be supported or clearly framed as general guidance

- No filler that reads like it was written for a search engine rather than a reader

This is why a generalist content agency typically underdelivers in insurance. The content quality floor is higher, and it shows up in rankings.

4. Off-Page SEO to Build the Authority That Gets You Ranked Over Bigger Competitors

Strong content on a solid technical foundation still needs external credibility signals before Google ranks it over more established competitors. Off-page SEO is how you build those signals.

- Link building

Getting credible websites to link to yours. In insurance, the most valuable links come from industry associations, local business directories, chambers of commerce, and regional publications.

- Digital PR

Earning media coverage or expert citations in publications covering business, finance, or local news. One credible placement builds more authority than dozens of low-quality directory links.

- Social media presence

Consistent activity on LinkedIn and relevant platforms signals an active, credible business. It also creates additional touchpoints with prospects who find you through search and check your social presence before making contact.

- Forums and community presence

Answering questions in industry forums, local business communities, and platforms like Reddit or Quora builds topical authority and drives referral traffic from people actively researching insurance options.

- Directories

Accurate listings in trusted directories (Google Business Profile, Yelp, industry-specific directories) reinforce local and category relevance. Inconsistent information across directories actively harms local SEO performance.

What SEO Can Do for an Insurance Broker When It Is Done Right

Before getting into the challenges, it helps to see the upside clearly. These are the business outcomes of well-executed insurance SEO, mapped to the metrics that actually matter.

| SEO Outcome | Business Impact | What to Measure |

| Ranking for local insurance queries | Inbound enquiries from prospects already searching for your services | Organic leads, form completions, website call volume |

| Google Business Profile visibility | Appearing in the map pack when nearby clients search for a broker | Map pack impressions, GBP calls, direction requests |

| Content that answers coverage questions | Prospects arrive pre-educated; shorter sales cycle, higher trust from the first call | Time on page, pages per session, lead quality |

| Outranking comparison sites on niche terms | Capturing high-intent clients searching for specific coverage types | Keyword rankings for niche and local terms, conversion rate by page |

| Building domain authority over time | Compounding organic traffic that grows without increasing ad spend | Domain rating, referring domains, month-on-month organic traffic |

| Reducing dependence on paid ads | Lower cost per lead as organic traffic grows; paid budget can be reallocated | Cost per organic lead vs. paid lead, SEO-attributed revenue |

Go to Google Keyword Planner and put your targeted keywords. You will see that almost all of your core keywords have Google Ads CPCs between $35 and $80. Over a 24-month horizon, that gap compounds significantly in SEO’s favour.

Why Insurance SEO Is Harder Than SEO for Most Businesses

Insurance SEO takes longer and costs more than SEO in most niches. That’s not a caveat, it’s a structural reality, and any agency quoting you the same rate they charge a restaurant either hasn’t priced in what the niche requires or will deliver the same output they’d give anyone else.

Three things make it harder than average.

Google Is Very Sensitive to Insurance Content Because it’s YMYL

Google uses a classification called “Your Money or Your Life” (YMYL). It applies to content that directly affects someone’s financial decisions or health outcomes. Insurance sits squarely in it.

Pages in YMYL categories are evaluated more strictly than lifestyle blogs or general service sites. Generic or thin content, even with technically correct on-page SEO, does not rank. What ranks is content that demonstrates real expertise, accurate information, and genuine credibility. Volume alone won’t move the needle in this niche. The quality floor is simply higher, and it applies to every page on your site.

You Have to Compete with Comparison Sites With Far More DA (Domain Authority)

For head-on terms like “car insurance quotes” or “best life insurance,” the top results are Policygenius, Compare.com, and national carriers. These are sites with enormous domain authority built over years. An independent broker will not outrank them on those terms, and a good agency won’t try.

The win is on specific, intent-rich, local queries: “commercial insurance broker for contractors in [city]” or “professional liability insurance for consultants.” Comparison sites don’t go deep on those terms. That’s where independent brokers can actually compete and win. Knowing which battles to fight is a core part of what separates insurance SEO from generic SEO strategy.

Insurance Content Needs to Be Genuinely Expert, Not Just Long

A 500-word explainer written by someone who can’t tell the difference between a broker and a captive agent, or who can’t accurately describe an umbrella policy, will not rank in insurance.

Google’s quality raters assess whether content reflects real expertise. A generalist content agency that doesn’t understand coverage types, underwriting basics, or how policies are structured will produce content that looks complete and performs poorly.

This is one of the most practical reasons to work with a specialist over a generalist. The content quality gap is hard to fake in a regulated, YMYL niche.

How Long SEO Takes for Insurance Brokers and What Affects the Timeline

Most insurance brokers see meaningful improvements in organic traffic within 6 to 9 months. Competitive queries, particularly for broad commercial insurance terms in larger markets, typically take 12 to 18 months. Those are honest averages, not worst-case figures.

What moves the timeline shorter or longer:

- Domain age and existing authority. A site live for several years with some backlinks will see results faster than a brand-new domain starting from zero.

- Starting content volume. A site with a few pages has more ground to cover than one with existing service pages and indexed content.

- Local vs. national competition. A broker in a smaller regional market faces different conditions than one targeting a major city. Local timelines are typically shorter.

- Technical starting point. Significant crawl errors, broken pages, or poor mobile performance all need fixing before rankings can move, and fixing them takes time.

- Review velocity on Google Business Profile. Fresh, genuine reviews accelerate local SEO performance more than most brokers realise.

SEO is a long-term organic growth channel. It compounds over time. Google Ads stops generating leads the moment the budget runs out. The organic traffic built through SEO remains and grows over time. The 12-month horizon can feel long, but the asset being built doesn’t disappear when you stop paying for it.

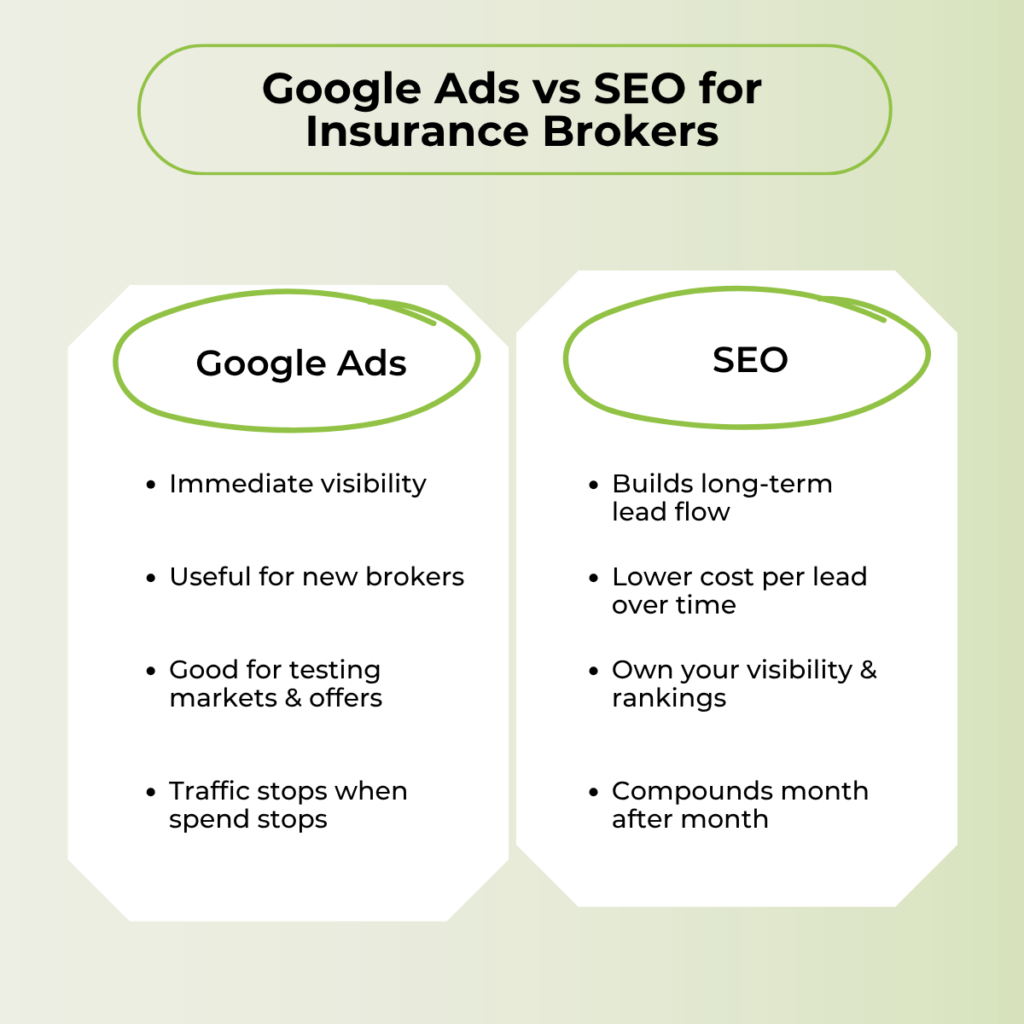

SEO or Google Ads, Which Makes More Sense for an Insurance Broker

Most brokers have run Google Ads, considered them, or are currently paying a lead aggregator that uses them to sell the same prospect to five competitors. The comparison matters…and in insurance, it lands differently than in most industries.

Run Google Ads If Any of These Apply to Your Situation

Google Ads has a specific role in insurance. It’s not a long-term strategy, but it has a legitimate short-term use:

- You just launched and need immediate lead flow while organic rankings build

- You’re running a time-sensitive campaign — open enrollment for health cover, a new product line, or a seasonal push into a specific vertical

- You’re entering a new market and need fast visibility in a city or region where you have zero organic presence

- You’re testing messaging before committing to long-term content built around a specific angle

If you pay between $35 to $80 per click for and you set $2,000/month budget, that’s 25 to 57 clicks. And unlike most industries, you’re often bidding against comparison platforms and national carriers who have far larger ad budgets. You rarely win on volume. You win by being highly specific about who you’re targeting.

Start Building With SEO When These Apply to Your Business

SEO is the right primary channel when the economics of paid no longer make sense, or when you’re serious about building something that doesn’t disappear with the budget:

- Referrals are your main source and you want a second channel that you control

- Your paid CPL is too high to scale profitably. This is a common reality in commercial and specialty insurance

- You’re tired of lead aggregators selling the same prospect to multiple brokers before you even pick up the phone

- You serve a specific niche or geography. A broker in “commercial insurance for [city] contractors” can own that term organically; a comparison site never goes that deep

- You want inbound leads from prospects who found you specifically, not ones distributed across four other brokers

For fintech and insurtech companies, the SEO case is even stronger. B2B financial audiences are expensive to reach through paid, sales cycles are longer, and the ROI of individual ad clicks is harder to measure. A fintech SEO agency that understands YMYL content requirements and the compliance constraints of financial messaging is a fundamentally different thing from a generalist running standard campaigns.

SEO vs Google Ads at a Glance

| Google Ads | SEO | |

| Time to first lead | Days | 6 to 9 months typically |

| CPC in insurance | $35 to $80+ | None |

| What happens when you stop | Traffic stops immediately | Rankings remain and compound |

| Lead exclusivity | Same lead sold to multiple brokers via aggregators | Prospect found you specifically |

| Suited for | Short campaigns, new launches, market testing | Long-term client acquisition |

| Long-term CPL trajectory | Stays high or rises with competition | Drops significantly over 24 months [PLACEHOLDER: STAT — organic vs. paid CPL benchmarks, BrightEdge or Search Engine Journal] |

What It Costs to Hire an SEO Agency for Insurance

Insurance SEO commands a premium over general SEO. YMYL compliance, content quality requirements, and specialist competitive research all drive the cost up. An agency quoting you the same rate they charge a local retailer is either not accounting for those requirements or will deliver work that ignores them.

Here’s what the different budget tiers actually get you in this niche.

| Monthly Budget | What You’re Getting | Best Fit For |

| $1,500–$3,000 | Basic on-page optimisation, keyword setup, light monthly reporting, minimal content | Brokers with a new site, no existing SEO foundation, low competition market |

| $3,000–$6,000 | Content strategy, technical fixes, Google Business Profile management, some content production | Small-to-mid brokerages building organic presence in moderately competitive markets |

| $6,000–$12,000 | Full content production, link building, compliance-aware writing, multi-location optimisation | Established brokerages, regional expansion, competitive city markets |

| $12,000+ | Multi-vertical content strategy, digital PR, AI search visibility, national competition | Insurtech and fintech companies, national brokers |

What you’re buying at $2,000 per month and at $8,000 per month are not the same product, even if both are labelled “SEO services.” The lower end typically covers reporting, light on-page maintenance, and keyword tracking. Meaningful content production and link building start at the mid-tier range. In a niche with a high content quality floor, the investment required to actually move rankings is higher than in most other sectors.

How to Hire an SEO Agency That Actually Understands the Insurance Business

The wrong agency will produce technically adequate work that misses the YMYL requirements, doesn’t account for the comparison site problem, and delivers generic content that won’t rank in a competitive niche. Having the right budget matters less than finding the right partner. Here’s how to tell the difference quickly.

The Questions That Separate Insurance SEO Specialists from Generalists

Ask these five in any agency conversation. The answers reveal a lot.

- “How do you approach keyword strategy differently for insurance?”

A generalist says: we target high-volume terms. A specialist says: in insurance we focus on specific, intent-rich local and niche queries because brokers can’t win on comparison terms…so we find where you actually can.

- “Who writes the content and how do you ensure accuracy on insurance topics?”

Generalist agencies often outsource to content mills with no industry knowledge. The output looks complete and falls apart on accuracy, which Google’s quality raters will catch.

- “How do you handle the YMYL classification in your content strategy?”

If they don’t know what YMYL means, they don’t understand why insurance content requires a higher trust standard than the average blog.

“What metrics do you report on and how do they connect to lead generation?” Traffic and rankings are inputs. An accountable agency reports on enquiries, call volume, and lead quality.

- “Can you show me insurance content you’ve produced that’s currently ranking?”

The proof is in the results, not the proposal deck.

Red Flags That Tell You They Don’t Know This Niche

These are specific, recognisable patterns. Walk away if you see them.

- They promise first-page rankings within 60 to 90 days. Insurance SEO doesn’t move that fast. Anyone who says it does either doesn’t understand the niche or is setting you up for a difficult conversation at month three.

- They don’t ask a single question about your specific services, target geography, or client type before proposing a strategy. A real specialist needs that information before they can say anything useful.

- Their content plan is volume-first: eight blogs per month with no discussion of research depth or accuracy. In insurance, eight mediocre posts a month is worse than two well-researched ones.

- They only report on traffic and keyword positions, never on leads, enquiries, or conversions.

- The senior who pitched you disappears after the contract is signed. The person managing your account has never spoken to you before.

You Might Have These Questions About SEO for Insurance Brokers

Most agencies see meaningful organic traffic improvement within 6 to 9 months. Competitive queries in larger markets typically take 12 to 18 months. Domain age, content starting point, and local market competition all affect the timeline significantly.

Not on broad head-on terms. But brokers can compete and win on specific, intent-rich, local queries that comparison sites don’t cover in depth. “Commercial insurance broker for contractors in [city]” is genuinely winnable. “Cheap car insurance” is not.

Both serve different roles. Google Ads delivers immediate visibility at a high cost per click. SEO takes longer but generates organic leads at a significantly lower long-term cost. For most brokers, SEO is the primary channel with Google Ads used tactically for specific short-term campaigns.

A generalist can handle the technical basics. But the content quality requirements in a YMYL niche, the comparison site competitive landscape, and the need for accurate coverage-specific writing mean generalist output routinely underperforms in insurance. Specialist knowledge is what the content needs to rank.

The Brokers Who Commit to SEO Stop Depending on Referrals Alone

Referrals are the backbone of most broker businesses. But they’re unpredictable. They depend on someone remembering to mention your name, at the right moment, to the right person. That’s not a lead channel you control.

But if you invest in SEO, you’ll start ranking in front of strangers who need you. AI models will start recommending you to your ideal prospects.

If you’re ready to build it, book a call with the Saiqic team or [read how we approach SEO content for financial services.